Computational Financial Statistics

The rapid increase of the volume of the financial derivative markets is leading to huge volumes of data and large numbers of transactions. This has created a need for new statistical tools that can deal with these huge data sets, while at the same time is consistent with the current state of art mathematical models used in finance.

Aims

The project is interdisciplinary in the sense that we use advanced numerical methods often unknown to statisticians to improve statistical algorithms for continuous time processes, commonly used in finance.

We will work on several problems, ranging from inference from option data to classical time series problems and with partially observed data.

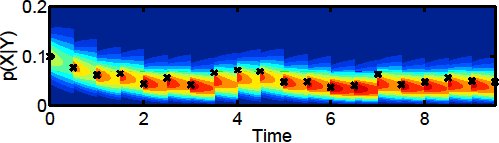

Methods

Parametric statistics compress information into a vector of parameters that summarizes the information. The most popular method for estimating parameters is the Maximum Likelihood (ML) method. The problem with that method is that the needed building blocks, the transition densities are given as the solution to a (possibly multivariate, nonlinear) partial differential equation. The computational cost for a single evaluation of the log-likelihood function will then be the number of observations. Optimizing the log-likelihood function typically takes a few hundred iterations… The computational cost is therefore significant!

We have therefore also considered simpler alternatives, such as the Quasi ML method, where we have shown that the computational cost is independent of the number of observations, a very substantial reduction.

Research group

PI:Doc. Lina von Sydow, Doc. Elisabeth Larsson, PI: Prof. Erik Lindström

Uppsala University

Dr. Josef Höök

Uppsala University

Links and references

- Höök, L. J., & Lindström, E. (2016). Efficient computation of the quasi likelihood function for discretely observed diffusion processes. Computational Statistics & Data Analysis. doi:10.1016/j.csda.2016.05.014

- Höök, L. J., & Lindström, E. (2016). Unbiased model selection for randomly observed diffusion processes. Submitted.

- A. Safdari-Vaighani, A. Heryudono, and E. Larsson, A radial basis function partition of unity collocation method for convection-diffusion equations arising in financial applications, J. Sci. Comput., 64 (2015), pp. 341-367. (pdf)

- L. von Sydow, L. J. Höök, E. Larsson, E. Lindström, S. Milovanović, J. Persson, V. Shcherbakov, Y. Shpolyanskiy, S. Sirén, J. Toivanen, J. Waldén, M. Wiktorsson, J. Levesley, J. Li, C. W. Oosterlee, M. J. Ruijter, A. Toropov, Y. Zhao, BENCHOP-The BENCHmarking project in Option Pricing Int. J. Comput. Math., 92 (2015), pp. 2361-2379.

- V. Shcherbakov and E. Larsson, Radial basis function partition of unity methods for pricing vanilla basket options, Comput. Math. Appl. 71 (2016), pp. 185-200.